Cui Bono?

The truth about the EU Reset's supposed £9 billion benefits

In May this year, the Prime Minister announced that the UK’s relationship with the EU would be ‘Reset’ and that this reset would benefit the UK economy by ‘nearly £9 billion’ by 2040, which he also claimed would be a ‘huge boost to growth’. Even the headline of the press release was misleading: ‘PM secures new agreement with the EU to benefit British people’, implying that the total population of the UK will somehow benefit, but the real beneficiary will be the EU, EU businesses and a handful of large multinationals.

The government would probably argue that their headline is justified because large multinational companies employ some ‘British people’, but it is unlikely that the companies’ British employees or their British customers will see any benefit from the ‘Reset’. However, British taxpayers will have to foot the massive bill for the Reset, which allows these companies to lower their export costs. This is yet another instance of businesses socialising their costs while keeping their profits. But why is a ‘Labour’ government helping them do this?

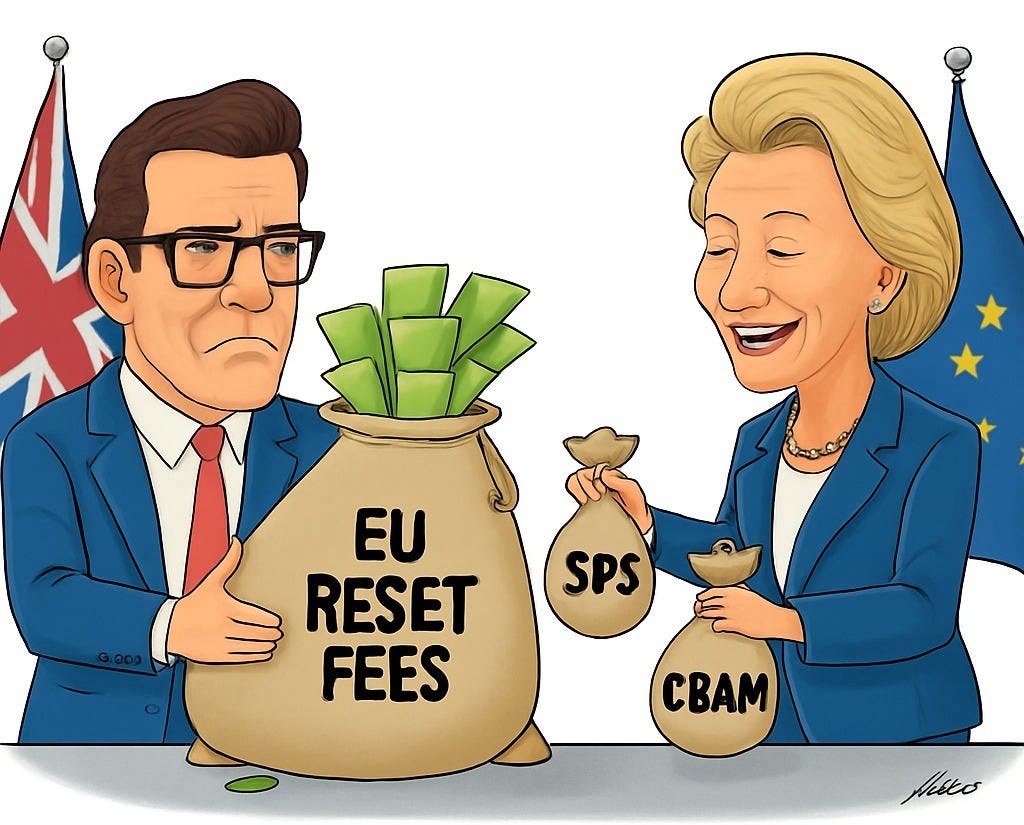

The Prime Minister claimed that £9 billion in benefits by 2040 would come from savings for exporting companies, which will be able to avoid paying EU carbon taxes and the costs associated with completing EU SPS forms. However, Starmer failed to mention that UK taxpayers would have to pay for these costs, and that the EU would also set our food and agriculture rules and determine our carbon price. The EU’s more factual publications on the Reset are extremely clear that the UK will have to pay to join the EU’s Sanitary and Phytosanitary (SPS) area, as well as its Emissions Trading Scheme (ETS) and Carbon Border Adjustment Mechanism (CBAM). But we have yet to receive the joining invoice.

We have, however, recently discovered the massive cost of joining some of the other schemes in the Reset: for example, joining the EU’s military procurement fund (SAFE), which does not guarantee any EU procurement from UK defence companies, could cost up to £5.7 billion to join and £132 million per year for administration. Meanwhile, the government has already agreed to give away the UK’s fishing waters to the EU for 12 years, which is estimated to cost up to £5 billion over the period, but some estimates put the cost as high as £9 billion if we count all EU catch value as forgone UK catch. Seafood is one of the UK’s only surplus agrifood exports to the EU. I doubt that Starmer included this loss in his calculation of ‘£9 billion in benefits’.

The time value of money

Recently, the £9 billion ‘benefit’ of the Reset has been repeated in the Pro-EU media, but the ‘by 2040’ date has been quietly forgotten. The pro-EU media also avoids the awkward question of whether this paltry annual sum of £600 million is gross or net of all other EU charges. To put that into context, £600 million is only 0.02% of the current UK GDP of £2.87 trillion. The OBR doesn’t estimate GDP out to 2040, but if we extrapolate from their medium-term baseline, UK GDP might be between £4.5 and £5 trillion by 2040. Either way, the so-called benefits are negligible and will be challenging to measure, as they are private company savings, not public savings. Additionally, there will be an associated loss of fees for export health certificates, which are issued by UK local authorities, not the EU.

I should also add that the £9 billion in benefits was not calculated by the OBR but by the Prime Minister’s Office. We can assume that it is a gross benefit, as the government is only just beginning to negotiate the costs of joining the EU’s SPS area and its ETS/CBAM scheme.

How much do other non-EU countries pay for the EU’s SPS area, food and agricultural regulations?

Other non-EU countries pay for EU SPS access via the Cohesion fund. For example, during the 2021-2028 EU budget period, Norway will contribute €3.17 billion towards the EU’s Cohesion Fund for its EU SPS area access. This is equivalent to approximately €453 million (£385 million) per year. Norway also contributes between €400 million and €500 million annually to other EU programs. Its total annual contribution to the EU is between €850 million and €950 million. However, as Norway, an EEA member, already complies with all EU SPS regulations, this fee is likely intended to preserve Norway’s agricultural export surplus with the EU. Norway exports approximately €7.4 billion in agrifood goods to the EU, predominantly seafood, and imports agrifood worth around €6 billion from the EU, which accounts for about 64% of Norway’s total agricultural imports. Norway does not pay to access the EU’s ETS and CBAM, as it has been a full participant in the EU ETS scheme since 2008.

Switzerland, an EFTA country, paid €1.2 billion towards the EU’s cohesion fund for the period from 2019 to 2024. However, from 2025 onwards, it will pay approximately €320 million per year, with the amount to be reviewed every seven years. In return for this paid SPS access, Switzerland aligns dynamically with most EU SPS and food safety regulations. Switzerland linked with the EU’s ETS scheme in 2020, so it is exempt from EU CBAM and did not pay an access fee to join the EU’s ETS scheme. However, the EU intends to charge the UK a fee to comply with EU carbon emission taxes, which would dramatically increase the costs of emissions for UK businesses.

How much would UK exporters have had to pay for EU CBAM on their products?

Starmer attempted to justify his £9 billion benefit calculation by claiming that the EU’s CBAM ‘would have sent £800 million directly to the EU’s Budget’ and that UK steel would have paid £25 million per year. Both figures seem far-fetched. And the £800 million would have come from UK exporting companies, not from the public purse.

The EU’s CBAM only covers six products: Iron and Steel, Aluminium, Hydrogen, Fertilisers, Electricity and Cement. None are significant exports for the UK. The UK’s largest steel export by weight is scrap steel, which would not attract a CBAM charge; however, it is mainly exported to non-EU countries with cheaper power for recycling. CBAM is calculated based on CO2 emissions, which vary by weight and manufacturing process, rather than by value.

Starmer didn’t mention that the UK was developing its own CBAM scheme, which would have protected UK industries, such as ceramics and glass, whereas the EU’s scheme does not. It protects industries important to the EU, such as steel and aluminium, but only for basic products, such as ingots, slabs, coils, sheets, bars, pipes, tubes, and rails. The EU’s CBAM will not be charged on the steel and aluminium used in finished complex goods, such as cars, trucks, bulldozers, aircraft engines, and washing machines, before 2030 due to the complexity of tracking emissions in these goods.

Starmer should be aware that the vast majority of UK steel and aluminium exports to the EU are in complex finished goods, rather than in base products, so UK companies’ CBAM costs for steel exports would be very low. The UK does export a small amount of aluminium to Germany. However, the UK’s only remaining aluminium smelter, located in Scotland, uses hydroelectric power; therefore, the company that produces it would have paid no CBAM on its exports to the EU. The UK has so little remaining base material manufacturing capacity, largely due to the UK government’s Net Zero policies, that it is easy to pinpoint where and how UK base materials are produced. Instead, the UK imports basic steel and aluminium from the EU, mainly from Germany, which still uses coal to generate electricity, to make into finished goods. But as the EU’s carbon price is higher than the UK’s, there would have been no UK CBAM to pay on imported German steel and aluminium either.

What about the costs for UK food exporters to export their goods to the EU?

Starmer also claimed that the UK should pay to join the EU’s SPS Area because UK agrifood exports to the EU had decreased by 21% and that our imports had decreased by 7% since Brexit. Trying to imply that this decrease was due to EU SPS rules, it isn’t; it is due to the rules of the EU-UK trade agreement. And his figures are not even correct.

Since the end of the transition period, UK SITC 0 Food and Live Animal exports to the EU have decreased by 14% while imports have decreased by 3%, according to the ONS, using CVM to account for inflation. Starmer also overlooked the fact that SITC 0 Food and Live Animal exports to non-EU countries increased by 4%, and imports increased by 14%. However, this Europhile Prime Minister is only interested in preserving ties with the EU, not with the benefits of total trade to UK consumers and producers.

If we look at the more detailed ONS analysis of Trade in goods: country by commodity, exports, the only falls in agrifood exports since Brexit to the end of 2024 are in SITC 05 Vegetables and Fruit: down 25%, SITC 21 Hides, skins and fur skins: down 24%, SITC 22 oil-seed & oleaginous fruits: down 50%, and SITC 29 Other crude animal & vegetable materials: down 25%. All of these export reductions pertain to products that were only ever transhipments to the EU from American, Asian and Commonwealth countries via UK ports and were miscounted as UK exports by the EU’s Intrastat system prior to Brexit. This phenomenon is known as the Rotterdam effect, and all trade experts are familiar with it. Now the government is trying to pretend the Intrastat figures were real. They were not! The UK does not produce tropical fruit, palm oil, or bamboo. Paying to join the EU’s SPS area will not change this. Transhipments of Caribbean bananas, PNG palm oil, Chinese bamboo and American almonds will never be counted as UK exports to the EU under the terms of the UK-EU trade agreement.

How much should the UK pay to the EU to let them make our food and agriculture rules?

The UK is not a significant exporter of agricultural food products. The UK imports significantly more agricultural and food products from the EU than it exports to the EU.

Browne Jacobson calculates that joining the EU’s SPS Area could potentially save UK agrifood exporters £200-£300 million annually by reducing the requirements for animal health certificates, quality assurance schemes and other export procedures. UK food importers could benefit by an additional £200 million per year from the Reset, according to trade consultancy, the Customs-Declaration.UK. In total, the benefits to UK agrifood importers and exporters could be £400 to £500 million a year, which is slightly more than the amount UK taxpayers would have to pay if the UK were to pay the same amount as Norway to join the EU’s SPS area.

However, the UK could be asked to pay much more than Norway for SPS access, as the UK exports more to the EU: in 2024, UK SITC 0 Food and Live Animal exports to the EU, measured in current prices, were £11.35 billion, equivalent to about €12.84 billion and 74% more than Norwegian agri-food exports. Therefore, the EU would likely require an annual payment of £690 million to access its SPS system. Dwarfing any potential gains.

If potential costs to taxpayers are approximately £700 million, but the benefits to food companies are only up to £500 million, the Reset could result in a net cost of £200 million to UK taxpayers. If we add the UK’s £39 billion food imports from the EU to its £11 billion food exports to the EU, the Reset would have added 0.4% to the UK’s total £50 billion agri-food trade with the EU in 2024.

More importantly, the people paying the Reset costs – the UK’s taxpayers – are not the same people as those who will benefit from lower agrifood trade compliance costs. And there is little chance that the benefits will ever be passed back to taxpayers.

So, who does benefit?

Of the UK’s top ten agri-food exporters, only one is owned by a UK farmers’ cooperative, while only two are listed on the LSE. All of the other companies being subsidised by UK taxpayers are massive, global, privately owned companies. Why are UK taxpayers subsidising their export costs to the EU? We don’t subsidise their exports to any other destination.

The UK’s top ten agri-food exporting companies to the EU are:

Associated British Foods – Baked goods – LSE listed, FTSE100.

Arla Foods UK – Dairy – Farmers Cooperative, subsidiary of Arla Foods amba, Denmark

Muller UK – Dairy – German family-owned group

Bunge (UK Operations) – Oilseeds and feed - NYSE listed

Cargil (UK) – grains and oils - Privately owned, US Cargill-MacMillan Family

JBS UK (2 Sisters Food Group) – poultry – Privately owned, Boparan Holdings Ltd.

Cranswick – pork, bacon and gourmet meats – LSE Listed, FTSE250.

Kepak Group (UK) - Beef and lamb – Privately owned, Irish, Kingate Investments.

Tulip (Danish Crown UK) – pork – private US-based company, majority owned by JBS S.A. Brazil. (formerly a Danish farmers’ co-operative.)

First Milk - Dairy – Private – UK farmers’ cooperative.

What about UK food Importers from the EU?

Like the Agrifood exporters, the list of the UK’s top ten Agrifood Importers from the EU is just as undeserving of taxpayer subsidies, although slightly more UK-focused:

Tesco – supermarket chain - LSE Listed FTSE100 – institutional investors 13% owned by Qatar Investment Authority.

Sainsbury’s – Supermarket chain - LSE Listed FTSE100 – 15% owned by Qatar Investment Authority and 15% by the Sainsbury family.

Asda – supermarket chain – privately owned by Issa Brothers and TDR Capital Private Equity, with Walmart retaining 5%.

Morrisons – supermarket chain – privately owned by Clayton, Dubilier & Rice private equity.

Aldi UK – supermarket chain – privately owned subsidiary of Aldi Sud, German-based Siepmann and Markus Foundations and Albrecht family descendants.

Lidl UK – supermarket chain – private subsidiary of Lidl Stiftung & Co. KG, privately owned by Dieter Schwarz and Schwarz family foundation, Germany.

Lamex Foods – privately owned food importer – meat, dairy, fruit and vegetables from EU countries – import value in 2024 £1.5 to £2 billion.

2 Sisters Food Group – privately owned by Boparan Holdings Ltd, the UK’s largest poultry processor and importer.

Greencore – LSE Listed – Irish-based company – manufacturer of convenience foods – imports £1 to 1.3 billion worth of fresh lettuce from Spain and the Netherlands, as well as dairy products and preserved meats from Ireland

Samworth Brothers – private family-owned company – manufacturer of Ginsters Pasties and Melton Mowbray pies, imports £0.8 to £1.1 billion pork, butter and onions from Ireland, Denmark and the Netherlands.

Protests about supernormal profits but not about supernormal subsidies

It is strange that there are a group of left-wing Labour supporting activists who believe that UK supermarkets are making Supernormal profits and ‘ripping off’ UK shoppers, but those same activists are silent about the UK government’s plan to pay the EU with UK taxpayers’ funds, what could amount to almost £700 million a year so that these supermarkets can make even greater profits. Where are the protests about supernormal subsidies?

A better solution

There have been efforts to blame higher food prices on Brexit, but many pro-EU activists and most politicians will be surprised to know how many minimum wage jobs are responsible for getting agricultural produce from the field or port, to the supermarket shelf: picking, washing, packing, processing, retail packaging, warehousing, deliveries, self-stacking and checkout operators are generally minimum wage jobs. The cost of all these jobs increased in April when Rachel Reeves raised the minimum wage and the employers’ National Insurance Contribution. This is why food costs have increased. It has nothing to do with Brexit, and the Reset would NOT change this.

Food companies also face significant energy costs due to the government’s Net Zero policies, which have contributed to increased industrial electricity prices. The electricity needed to run packaging and processing factories, refrigerated storage warehouses and open-sided refrigerated shelves in supermarkets costs more in the UK than in any other developed country.

If this government wants to help UK food companies, it should remove its taxes on industrial electricity and reverse its NIC increase on minimum wage employment. Instead, Starmer wants UK taxpayers to pay the EU to make UK food and agricultural regulations, so that his government doesn’t have to do the job it was elected to do. Starmer believes that reducing the trade compliance costs of food companies trading with the EU will compensate for the additional costs his government has imposed on them through higher taxes on energy and employment. It won’t. It won’t help UK farmers or food producers either. It will just make importing food from the EU cheaper, which could reverse the market share gains UK food producers have made since Brexit. Since Brexit, UK food self-sufficiency (production to supply ratio) has increased from 60% in 2020 to 65% in 2024, while the indigenous food production to supply ratio has increased from 74% to 77%. Why would the government want to reverse this to slightly reduce the costs of some large multinational companies?

Loss of Sovereignty

The Reset is not just about the cost to UK taxpayers; we are also giving up our ability to make our own rules so that a handful of supermarkets and multinational agricultural companies can reduce their costs when trading between the UK and the EU. The Reset will prevent UK farmers from using new technology unless the EU has approved it. The Reset will prevent the UK from making its own animal welfare rules. The Reset will prevent the UK from determining its own food safety regulations. The Reset will drive UK manufacturers out of business by forcing them to pay the same amount for their carbon emissions as EU companies, even though UK industrial energy costs are higher than those in the EU due to our environmental charges and taxes. The Reset will also allow EU unemployed youth to enter the UK, potentially taking away opportunities from young people in the UK.

It is time to say No, to the Reset. If for no other reason, we can’t afford it.

Another brilliant and very well researched post by Catherine. Pity that Starmer will not read it, although one doubts that he could follow it even if he did.

Thanks Robert